Is the Webtoon Market Shrinking?

Speaking for my own job security, I hope not.

Earlier this year, the Korean Creative Content Agency announced that the South Korean webtoon industry had reached an impressive milestone, hitting 2 trillion KRW (~1.36 billion USD) in revenue.

This isn’t happening in a vacuum, on the contrary the webtoon industry has grown for 6 consecutive years, boosted no doubt in part by COVID and a slower adoption rate to digital by existing comics and manga publishers.

Just this past May, Kidari Studio reported the highest Q1 revenue they’ve ever seen for their webtoon business, 158.41 billion KRW, driven by an increase in sales outside of Korea (61.932 billion KRW). For their part, WEBTOON reported a staggering 325.7 million USD in sales during the same period. We haven’t even brought up RIDI hitting a record high revenue of 235.4 billion KRW in 2024 driven heavily by their domestic sales, but also by advances in their North American service, Manta.

Everything looks great, right? Right?

The Fly in the Ointment

While press releases tout the revenues of webtoon platforms, many of them are operating in the red and have been for years. Kidari Studio’s overseas sales increased for Q1 while domestic sales actually shrank. The end result? Kidari Studio’s losses for their webtoon division were 8.13 billion KRW. Their merchandising sales made up for those losses with a 13.605 billion KRW profit bringing the company into the black.

Naver WEBTOON’s operating loss was 26.634 million USD, dwarfing the Q1 figure from 2024 (14.188 million USD). And RIDI saw an operating loss of 12.9 billion KRW in 2024 bringing them squarely into the red when it comes to not just their webtoon division, but the company as a whole.

Luckily, Kidari and Naver are both conglomerates able to absorb the losses. Or, better yet, their overseas platforms were established early enough that they have a loyal fanbase and strong brand to weather the storm. RIDI might not have the deep pockets of the others, but they aren’t stretched thin over multiple languages and locales.

But there are plenty of platforms and businesses that weren’t as lucky.

This brings us to the list.

One Door Closes… Then Another, and Another

This section’s long enough without an introduction. So, here we go.

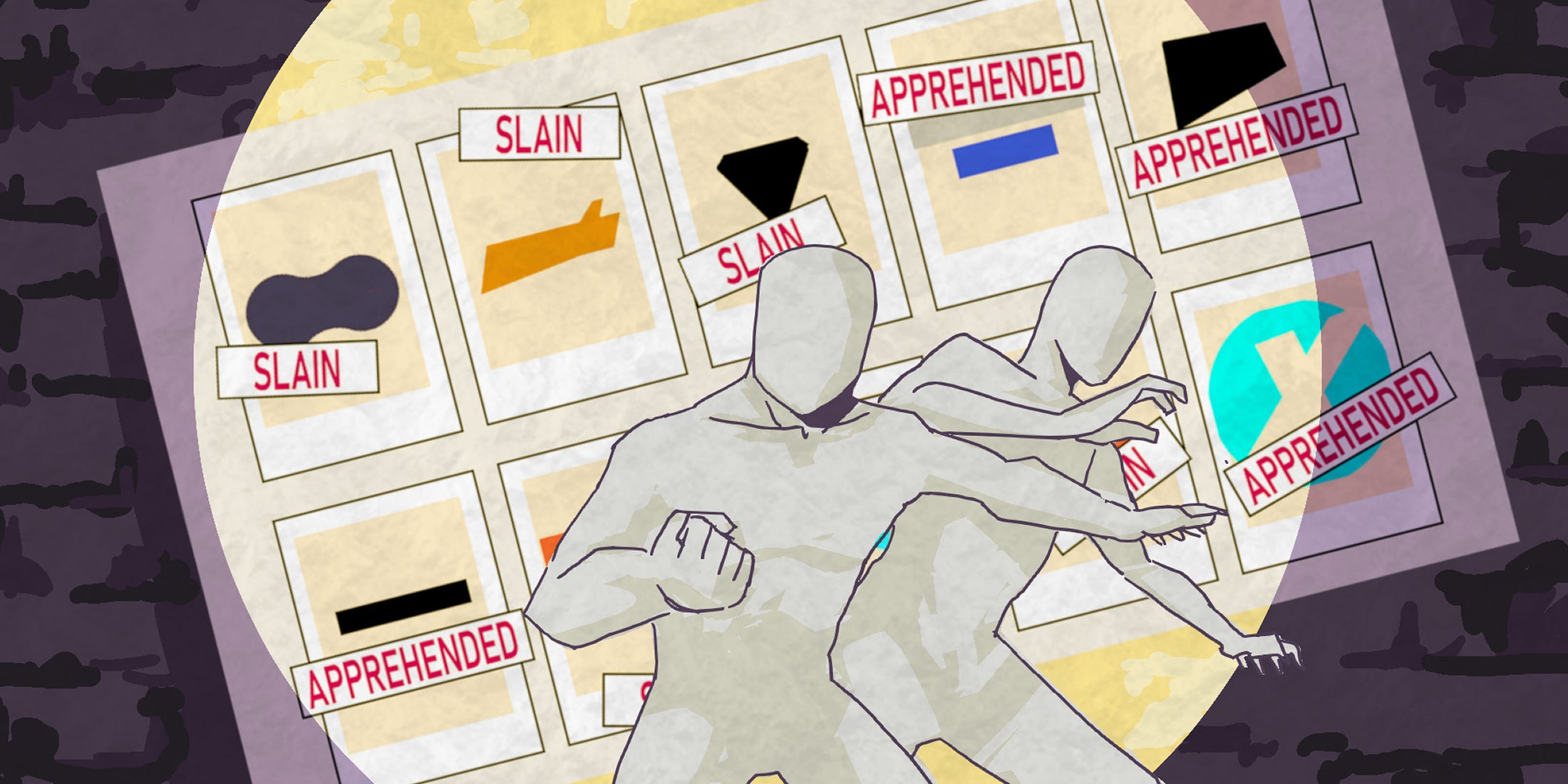

Kakao Piccoma announced the closure of Piccoma Europe, their French platform and the biggest competitor to WEBTOON in France, back in May of 2024 (JoongAng Daily). The platform launched in March of 2022 and was focused on publishing translated versions of Korean webtoons for the French market and was incredibly active in the French market until last year.

Then, in October, Kakao Piccoma announced they would be withdrawing from the Indonesian and Taiwanese markets as well in order to focus on North America and Japan (Maeil Business). The Taiwanese market was likely due to lack of growth while piracy was given as the main reason for Indonesia.

In November, NHN announced they would be closing their platforms in Taiwan and Germany (Business Korea). This was after they had already sold their Thai Comico subsidiary to Kidari Studio and left the Vietnamese market in 2022. This left their South Korean and Japanese businesses under the Comico brand and North American and French businesses under the Pocket Comics brand (more on this later).

In Korea, the longstanding Peanutoon platform announced their closure back in February after many years of service (Ilbo). Only a few days later, some of the titles were contracted onto Kidari Studio’s Bomtoon service while others were in limbo due to contract terms with the operator of Peanutoon, Nexcube.

This came only a few days after RIDI announced the closure of OrangeD, a webtoon studio owned and operated by RIDI. They were responsible for a great deal of popular BL webtoons on the Manta and Lezhin platforms (Newsway) including Killer Crush and Punch Drunk Love.

In March, Studio YesOne’s closure, which was announced in 2024, was completed and the studio completely dissolved (Seoul Webtoon Insight). Studio YesOne was a joint venture between Yes24, an online bookstore, and the One Store, a digital app store. The studio was designed to utilize Yes24’s offline distribution channels as well as the One Store’s digital distribution experience, but it never came together.

Then, in April, Kidari Studio announced the closure of KDKD, their NFT marketplace. It wasn’t a major surprise considering the lack of popularity web3 and crypto has in the webtoon industry, but it was a significant event nonetheless.

Of course, April had bigger news that far overshadowed the closure of an NFT platform. Kakao was rumored to be preparing Kakao Entertainment to be sold off in a letter to shareholders (JoongAng Daily). KE owns and operates content services like Kakao Webtoon, Kakao Page, Tapas, and Radish and owns shares of Starship Entertainment, SM Entertainment and more. Since then, KE has actually opened a new headquarters in Los Angeles so… who knows how true these rumors are.

Just last month in May, Bufftoon announced their closure (This is Game). While the platform was home to popular webtoons in the past, it was in direct competition with Naver Webtoon and while NCSoft might be a giant in games publishing, they weren’t making it in the webtoon industry.

And finally, just a few days ago, NHN was heard to be considering the closure of their European webtoon operations with the closure of Pocket Comics France (Maeil Business). This would leave their operations in Japan, Korea and North America with only the NA platform operating under the Pocket Comics brand.

WHAT.

Under the circumstances, it was probably inevitable that the webtoon industry would enter correction territory. Most of the industry agrees that the most stable markets outside of Korea are Japan and North America. Both of which have a much longer history with webtoons than Europe or Southeast Asia.

More than that, there was a definite rush to replicate the successes of North America and Japan in Europe. While most platforms in North America started with 8 - 10 new launches per month, European platforms were hitting 20+ right out of the gate. That, combined with marketing costs and expedited ROAS projections led to difficulties meeting goals.

Here at home, Korea saw a second culling of studios and publishers, similar to what we saw in 2017 - 2018. But, in the same time period, we’ve seen multiple studios cement their position in the industry including Lezhin’s Studio M, TOPCO’s Japanese ventures, not to mention Naver’s own investments abroad like Studio No. 9.

So… Is the Webtoon Industry Shrinking?

Yes, but for the better.

Post-COVID, there was a rush to expand into international markets. Most of the overseas platforms that closed in the past year (really, the past 2 years) were opened during that initial gold rush. And outside of the officially closed platforms, there are a host of others that never closed but are barely supported.

Now that the dust is beginning to settle, we’re seeing more local platforms and publishers make the move into webtoons. In France alone, we have the webtoon platform ONO, as well as print publishers like Komogi, Koda, Pika Editions, and KBOOKS to fill in the void left by Piccoma Europe and Pocket Comics.

I think, maybe, I should adjust my answer.

The Korean webtoon industry is shrinking, leaving room for more international players to get in the game. Whether it be Indoesian studios, North American print distributors, or independent studios in Europe, there’s more opportunity now than there was before as Korean companies start to pull back into “safe” markets.

Then, again. Maybe not.