Naver Rises while Kakao Looks For a New Way Forward

Q1 2025 Statements for Naver and Kakao have released in Korea

The first quarter statements for Korean companies are slowly being released, but the two biggest companies of note, Naver and Kakao, have both released their own wildly different statements.

Naver Rises, but Investors are Unimpressed

Naver’s revenue is separated into five categories: search platform, commerce, fintech, content, and enterprise.

Search platform: 101.27 billion KRW (11.9% YoY)

Commerce: 78.79 billion KRW (12% YoY)

Fintech: 39.27 billion KRW (11% YoY)

Content: 45.93 billion KRW (2.9% YoY)

Enterprise: 13.42 billion KRW (14.7% Yo)

The overall revenue is 278.68 billion KRW which represents a 10.3% YoY increase compared to Q1 2024. Noticeably, the search platform saw some of the largest increases due Naver implementation of AI-based optimizations in ad efficiency while their launch of the Naver Plus Store and continued enhancements to their online shopping/delivery business has resulted in continued growth.

The biggest sign that Naver is showing continued and sustainable growth is their operating profit for Q1 which was reported as 50.5 billion KRW, an 15% increase on Q1 2024.

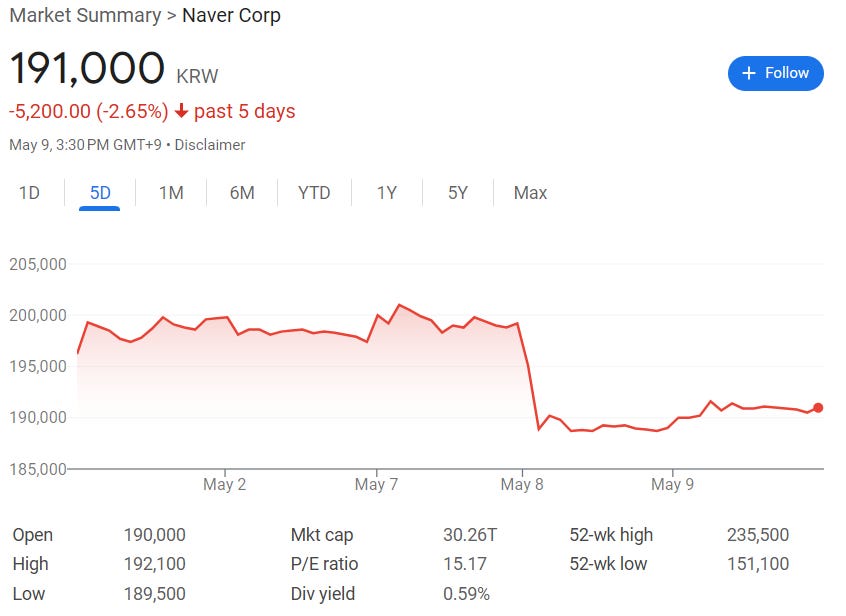

Whie the company is showing growth, it’s obviously not what domestic investors are hoping for as the stock is trading at ~191,000 KRW per share, down from the 200,500 KRW peak we saw last week. This is partly due to domestic investors drawing comparisons to international contemporaries like Google and their relatively quicker adoption of new technologies, namely AI.

Kakao’s Strategy Shift

Kakao’s own financial reports are slightly different from Naver’s in that the divisions are shown in slightly more details which allows investors to do a better job of discerning which operations are showing promise and which… well, I’ll let you judge for yourself.

Platform Division

Talk Biz: 55.3 billion KRW (7% YoY)

Portal Biz: 7.4 billion KRW (-12% YoY)

Other: 36.6 billion KRW (3% YoY)

Contents Division

Games: 14.5 billion KRW (-40% YoY)

Music: 43.8 billion KRW (-6% YoY)

Story: 21.3 billion KRW (-6% YoY)

Media: 75 billion KRW (-21% YoY)

Kakao’s Q1 overall revenue was 186.4 billion KRW which represents a 6% drop from the same period last year.

Kakao’s troubles have been well known for quite some time with the closure of Piccoma’s European and Indonesian platforms as well as the most recent rumors that Kakao Entertainment was being readied for sale.

For every article about Naver WEBTOONS’ growth in overseas markets, there’s a noticeable silence from Kakao Entertainment. The lack of competitiveness in the Japanese market, where Piccoma has the homecourt advantage, is a large cause for concern as well as Kakao’s own issues with promoting Kakao Page and Kakao Webtoon at home.

Most recently, Kakao has mentioned a larger strategy moving forward by centering the business around KakaoTalk. KakaoTalk is undoubtedly Kakao’s most successful product and one that they’ll be leveraging in an attempt to boost revenue in other sectors.

What Does this Mean for the Webtoon Medium?

It sounds an awful lot like Naver will be focusing heavily on foreign markets for the duration of 2025 while Kakao might have to focus on Korea and Japan for the time being. Naver’s current content strategy is well-known with multiple forays into film, anime, and print planned throughout the year while Kakao’s refocus on KakaoTalk leaves most western markets out in the cold.

I wouldn’t expect Tapas to change tactics anytime soon, but the content that gets promoted on it might start to shift as Kakao’s own internal compass shifts in accordance with their KakaoTalk audience’s tastes.

But, with Kakao’s renewed focus on the Asian market, that leaves the potential for competitors like Kidari Studio and Ridi to drive past overseas platforms like Tapas in the western market.